I Have Been Denied Credit

If you have run into issues of hoping to start building credit, but have been denied credit cards over and over, there are a few options you have. Applying or inquiring for more and more credit is not helping your scores. You can try a few other options such as:

- Applying for a Secured Credit Card

- CD Builder Loans

- Second Chance Checking

You can look for other options for credit cards here

What My Credit Score Says

Your credit score tells a lender the likelihood of you to default on a loan in the next 12 months. Credit demonstrates your trustworthiness to pay your bills and loans on time. Keeping this in mind, it is easier to understand what your credit report says about you as a borrower.

If you have late payments, this impacts your score significantly.

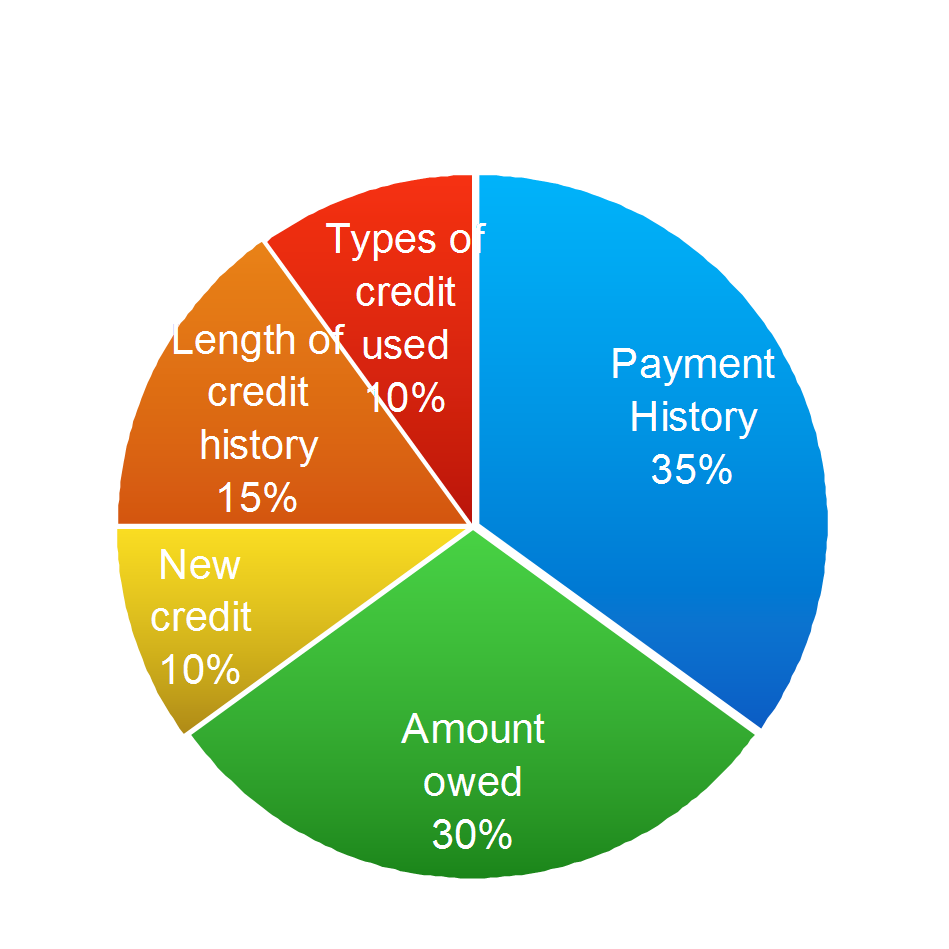

If you look at the chart above, you notice that your payment history makes up 35% of the FICO score. Therefore a late payment will tank your score! Another large portion of the FICO score rating, is the amount you owe. If your credit card balances are high, the easiest and quickest way to start improving your score is to pay your cards down as low as you can, rather than making the minimum payments.

In order to have a healthy credit profile, it is recommended to have two lines of revolving credit, and two personal (like home and auto) loans. If you have questions about other reasons your scores may be low or would like to speak with an attorney today, please call 1-800-994-3070![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]() . We would be happy to assist you further or answering any questions you have concerning your score.

. We would be happy to assist you further or answering any questions you have concerning your score.

A Note From The Author: The opinions you read here come from our editorial team. Our content is accurate to the best of our knowledge when we initially post it.

Article by Breana Washington