You’ve checked your credit score a dozen times this year. You’ve read the tips, maybe even tried a few. But you’re still not sure what all the effort is really for.

You might be thinking, “What’s the point of trying to improve this number if it doesn’t change anything right now?” Or maybe, “I’ve already made mistakes—there’s no way I’ll ever get it high enough to matter.”

Here’s the truth: your credit score is more than just a number. It’s a tool. And when you know how to use it, it can open doors you didn’t even know were closed.

Over the years, I’ve seen people go from rejected and discouraged to buying their first home, refinancing a car loan with better terms, or finally being approved for something without needing a guarantor. It’s not magic—it’s just the ripple effect of better credit.

In this article, you’ll see exactly what that looks like. Not through financial jargon, but through real-life, everyday wins that start with one simple shift: improving your credit.

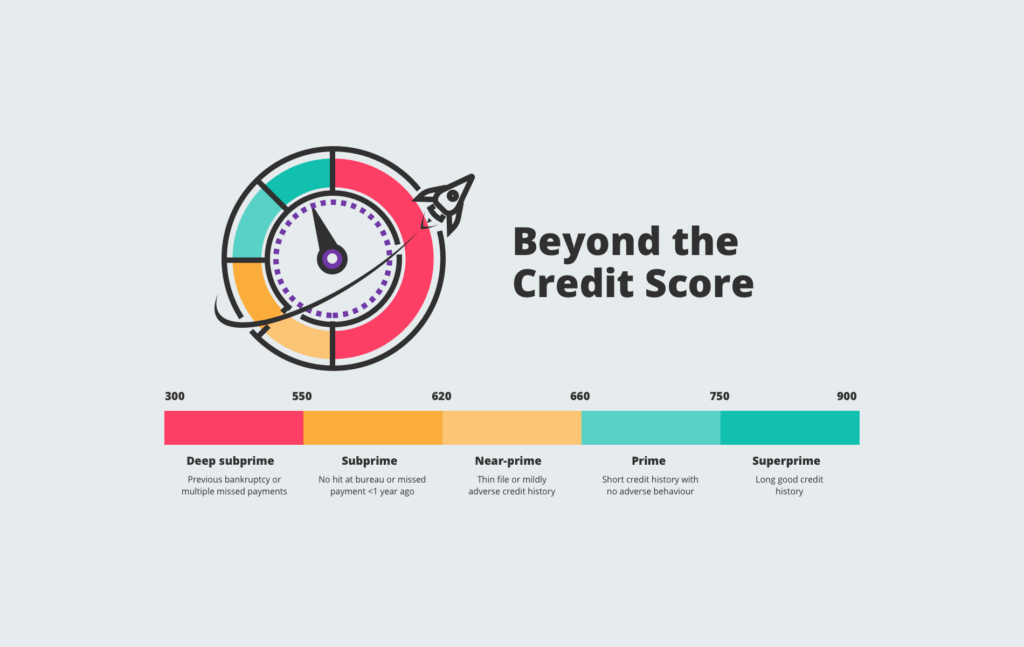

What most people misunderstand about credit

Most people think credit is all or nothing. Either you’ve got “good credit” or you don’t. And if you don’t? Well, then you’re stuck with sky-high interest rates, rejections, and disapproving looks from lenders.

But that’s not how it works.

Here’s the truth: improving your credit even a little can make a big difference. You don’t need a perfect 850 score to unlock better financial options. Often, just moving from “fair” to “good” can mean qualifying for better rates, reducing upfront deposits, or getting approved where you would have been declined.

The problem is that credit often feels like a black box. You make a payment—nothing changes. You pay off a card—your score dips. It’s confusing, and it can feel like you’re playing a rigged game.

But once you understand what your credit score actually influences, it starts to feel a lot less abstract. It’s not just about getting a loan—it’s about getting a loan that doesn’t cost you thousands extra. It’s about saving money month after month without doing anything differently—except having better credit.

Think of your credit score as your financial reputation. You don’t need to be perfect. You just need to show lenders—and the systems behind them—that you’re trustworthy enough to take a chance on.

And that small shift? That’s where the real-life benefits begin.

Scenario #1: The Mortgage Difference

Let’s say two people apply for the same mortgage. Same deposit, same house price, same job stability. The only difference? One has a credit score of 665. The other? 725.

You’d think the gap is minor. But here’s how that plays out in real life:

The person with the higher score could get an interest rate that’s half a percent lower. That doesn’t sound like much—until you do the math. On a $250,000 mortgage over 25 years, that small difference could save them over $20,000 in interest.

And that’s not all.

With better credit, they’re more likely to:

- Get approved by more lenders, giving them more options

- Avoid needing a larger deposit to “offset risk”

- Close faster, because their application moves through more smoothly

Meanwhile, the person with the lower score might have to accept whatever terms they’re offered—or get rejected entirely and delay buying altogether.

And the kicker? That 60-point gap is often the result of a few small changes: paying down a credit card, correcting an error on their file, or consistently making payments on time for a few months.

It’s not about being perfect—it’s about being in a stronger position when it matters. When you’ve worked hard to save for a deposit or find your dream home, your credit score can be the difference between “we got the keys!” and “we’re still waiting.”

Scenario #2: Car Finance Freedom

Picture this: you’re standing in a car dealership, eyeing a reliable used vehicle that fits your budget. You’ve got a steady income, some savings for a deposit, and you’re ready to drive away. But then your finance application comes back with two options:

→ A high-interest deal with painful monthly payments

→ Or a flat-out rejection.

All because of your credit score.

This is more common than you might think. Lenders use your credit profile to decide how “risky” it is to lend to you. If your scores on the lower end, they either say no—or offset that risk by jacking up your interest rate.

Now flip that scenario.

Let’s say you’ve spent the last six months improving your credit—paying down old debt, getting your accounts in order, and avoiding late payments. You walk into that same dealership, and now?

→ You’re offered a competitive rate, lower monthly payments, and more choice.

→ You can afford a better car or save money every month—without changing your budget.

→ You walk out feeling in control, not at the mercy of whatever deal they’ll give you.

For many people, this moment is a turning point. They realize it’s not just about whether they get approved—it’s about how good the approval is. That freedom—to choose the car you want, not just the one you can get financing for—is one of the most immediate, practical wins of better credit.

Scenario #3: Insurance & Everyday Wins

This is the part no one really talks about—how your credit score affects everyday costs you probably didn’t realize were connected to it.

Let’s start with insurance.

In the UK, while insurers can’t directly use your credit score to set your premium, they can and do use something called credit-based insurance scoring. It’s a way of estimating risk, and it can affect what you pay—especially for car and home insurance.

That means two people with identical driving records and addresses could get very different quotes—simply because one has better credit. And it doesn’t stop there.

Here are a few other everyday wins that come with better credit:

- No (or lower) upfront deposits on utility bills or phone contracts

- More options for “pay monthly” deals—without needing a guarantor

- Better credit card perks, like cashback or travel rewards

- Access to 0% finance offers for appliances, furniture, even holidays

These aren’t luxury perks—they’re ways to make your money go further, every month. And when you’re not being penalized at every turn just for your credit history, everything feels a bit more manageable.

The real win? Peace of mind.

You’re not constantly wondering if you’ll get approved or bracing for a worse rate than advertised. You just move through life with less friction—and more freedom.

Real Results: A Client Success Story

“I never thought my credit would hold me back so much. I was paying hundreds more in interest every year—just because of a few missed payments from years ago. But once I started working on it, things changed fast. Within nine months, I qualified for a better car finance deal, got approved for a credit card with rewards, and saw my insurance premium drop. I finally feel like I’m in control again.”

— Sarah B.

Sarah’s story isn’t a one-off. It’s what happens when your credit starts working for you, not against you.

Take the First Step

If you’re tired of being penalized for your past, it’s time to do something about it. You don’t need a perfect score—you just need a better one than you have now