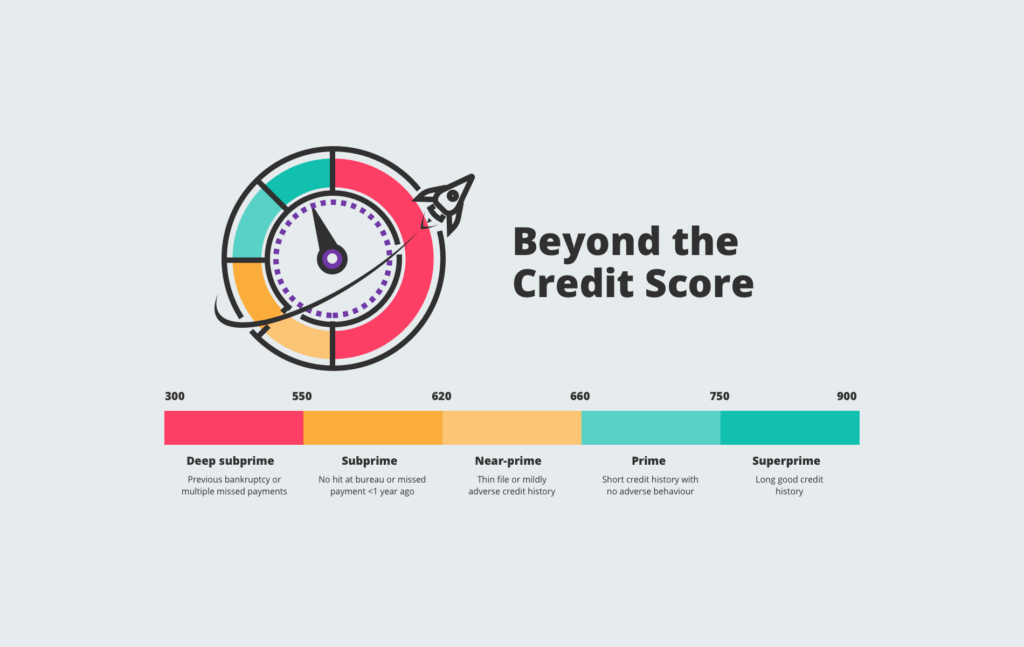

The average U.S. credit score has dipped to 715, according to FICO’s April 2025 Credit Score Insights. While this still falls within the “good” range, it marks a two-point drop year-over-year — the steepest decline since the Great Recession. For many Americans, this shift is more than just a number; it’s a signal that financial […]

14

Jul

Jul

Receiving a court summons for an unpaid debt can feel overwhelming. What started as a financial challenge can quickly escalate into a legal crisis — with potential consequences like wage garnishment, a judgment on your credit report, or even asset seizure. Creditors and debt collectors file hundreds of thousands of lawsuits every year, often hoping […]

09

Jul

Jul

So now is the time. You’ve been dreaming of becoming a homeowner. Striking out on your own. Building your own equity. No longer wanting to continue contributing to your landlord’s wealth in your monthly rent payments! This thrilling news and a major positive life stage! But what if you are like millions of Americans that […]

02

Jul

Jul

For many people, especially young adults, a credit score is something they rarely think about until an important financial opportunity comes along. Whether you’re applying for your first mortgage, financing a vehicle, qualifying for lower insurance premiums, or even interviewing for certain jobs, your credit score can quickly become one of the most important numbers […]

Collections, Credit Repair Blogs, Debt Collection, Scams

Debt Collection Letter for a Debt You Don’t Owe? Here’s What You Need to Do

30

Jun

Jun

Imagine opening your mailbox and finding a debt collection notice for an account you’ve never seen before. You don’t recognize the creditor. You never opened the account. Yet the collection agency claims you owe hundreds—or even thousands—of dollars. Unfortunately, this scenario is becoming increasingly common. At Credit Law Center, we regularly help consumers who discover […]

25

Jun

Jun

The People Behind The Credit Score At Credit Law Center we fully believe in the people behind the credit scores. A company is only as good as its “Why” and what matters to us most, is our clients. We recognize that bad things happen to great people and wish to help improve individuals buying power, […]

18

Jun

Jun

Millions of Americans with student loans are facing one of the biggest repayment changes in years. For many borrowers, this is not just a policy update. It may affect monthly budgets, credit reports, collection risk, and long-term financial plans. At Credit Law Center, we believe the most important thing borrowers can do right now is […]

Credit Repair Blogs, Credit Score, Student Loans

Credit Scores Are Dropping Nationwide: Why Legal Credit Repair Matters More Than Ever

11

Jun

Jun

A strong credit score is the foundation of financial stability—impacting everything from mortgage approvals to affordable interest rates. But recent data reveals a troubling trend: credit scores are falling across multiple states, creating what experts call a “perfect storm” for American wallets. For consumers, this isn’t just a statistic—it’s a wake-up call. What’s Happening? According […]

04

Jun

Jun

You’ve checked your credit score a dozen times this year. You’ve read the tips, maybe even tried a few. But you’re still not sure what all the effort is really for. You might be thinking, “What’s the point of trying to improve this number if it doesn’t change anything right now?” Or maybe, “I’ve already […]

02

Jun

Jun

Introduction Ever wonder if an account is too old to still be on your credit report? You’re not alone. A lot of people assume their credit reports are 100% accurate, but here’s the truth: mistakes happen, and old accounts sometimes stick around long past their expiration date. If you’ve got a debt from years ago […]