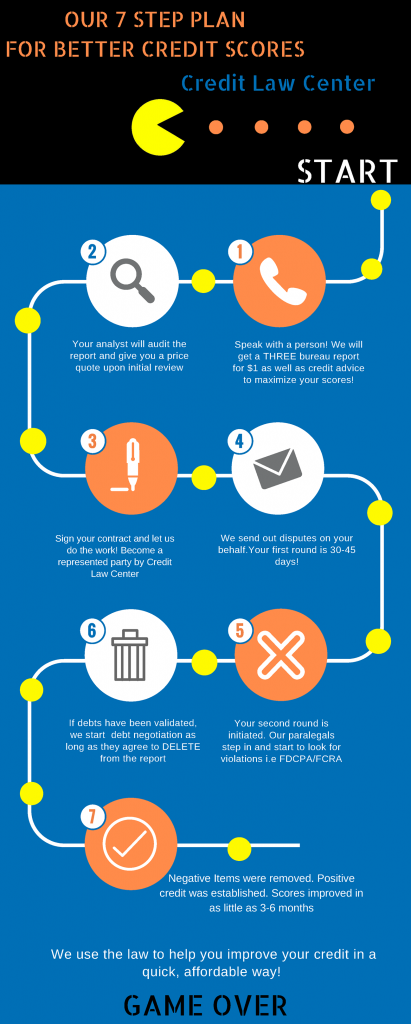

So You’re Saying There’s A Chance? All jokes aside, credit repair is a very serious matter. We have come into contact with many companies that over promise and under deliver when it comes to the services they offer. Have you been teetering back and forth between companies but have been unsure what to ask? Well […]

Monthly Archives: February 2020

20

Feb

Feb

How Do Inquiries Impact My Score? One of the common misconceptions about a credit score is that inquiries have a major role in the score. If you have looked at your credit score recently and feel that there are not many dings to the report that would cause your score to be low, take a […]

14

Feb

Feb

So you want to buy a house, but your credit score is 675 instead of 720 which will get you the best rate on a home loan. If you want to raise your credit score quickly, there are some steps you can take that can guarantee an exceptional home loan or any other credit line […]

13

Feb

Feb

Finance and User Friendly Apps If you do not watch a ton of television consider yourself lucky. Most commercials now are all about new apps and cell phones coming out. I am so far behind in I-Phones, I may as well just get a new kind of cell phone all together. With everything switching over […]

13

Feb

Feb

Finance and User Friendly Apps If you do not watch a ton of television consider yourself lucky. Most commercials now are all about new apps and cell phones coming out. I am so far behind in I-Phones, I may as well just get a new kind of cell phone all together. With everything switching over […]

11

Feb

Feb

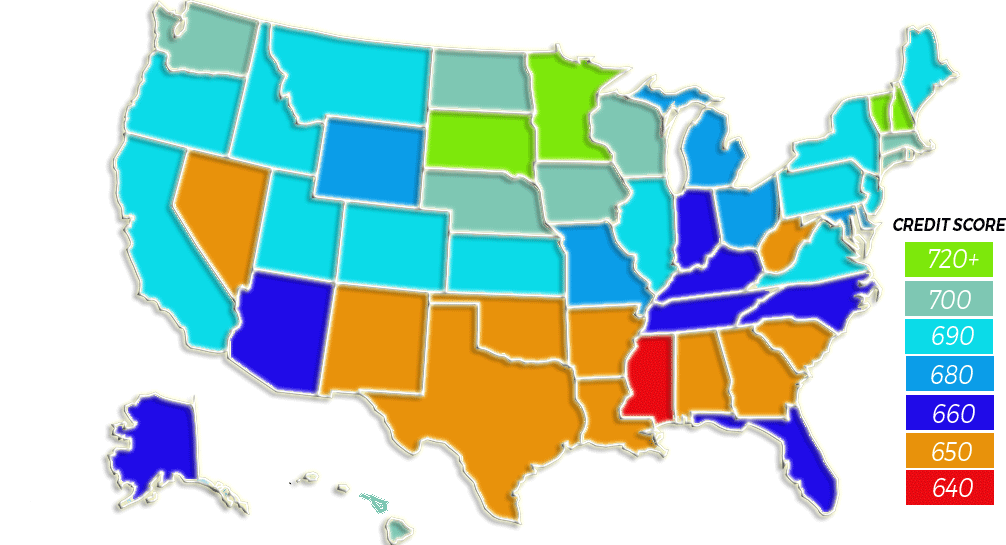

A Record-Breaking Year We have seen the highest average credit score ever in 2019 and the numbers keep rising! The U.S. economy is truly booming: Record job growth caused unemployment rates to drop to a record low and the stock market flourished throughout the year. Consumers showed their confidence as they continued to […]

06

Feb

Feb

The Major Questions While working at Credit Law Center and speaking with many of you over social media, I have been asked many questions over the credit repair process. Below I have posted the top questions and my answers to help get you started on the road to better credit! Question #1: “Why […]

03

Feb

Feb

A Road Map For Building Credit How to Establish a Good Credit Score Whether it’s finding a home for your growing family, financing your dream car, entering a career or even attempting to acquire a decent rate on car insurance, everything in our lives revolves around credit. No matter what you do, someone is […]