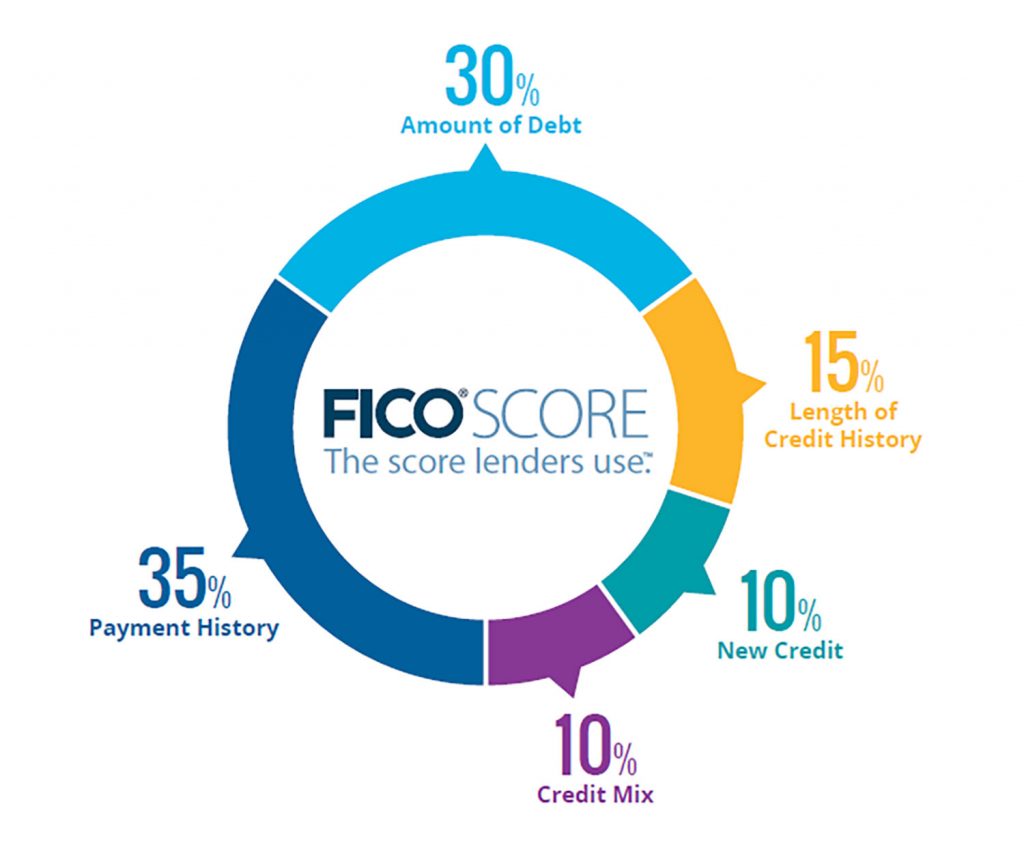

How Do Negative Items Affect Me? Negative items on your credit report could be what separates you from that home loan you hoped for or a decent financing for a vehicle. The good news is that if you happen to have these negative items on your credit report, there are still wats to mitigate their […]

Monthly Archives: February 2021

15

Feb

Feb

has almost been a full year since we heard the phrase “Two weeks to slow the flatten the curve” and the effects of the current pandemic had reached everyones lives in one way or another. For many Americans, this past year has tested the metal of their financial practices; providing questions without answer to their […]

08

Feb

Feb

Credit Alerts Worth Setting Up Now In order to maintain great credit scores, keeping track of all the activity on your accounts is key! Smart phones are attempting to make our lives easier with a multitude of applications. All major banking institutions now have online banking or apps to make life easier on their customers. […]