Combating Credit in this Era Let’s start out by saying what everyone already knows, the credit system is flawed and predatory in many ways. The concept of paying back what you have borrowed is pretty straightforward and providing an incentive to pay back your debts is needed, but how credit affects your life outside of […]

Monthly Archives: September 2019

13

Sep

Sep

Combating Credit in this Era Let’s start out by saying what everyone already knows, the credit system is flawed and predatory in many ways. The concept of paying back what you have borrowed is pretty straightforward and providing an incentive to pay back your debts is needed, but how credit affects your life outside of […]

11

Sep

Sep

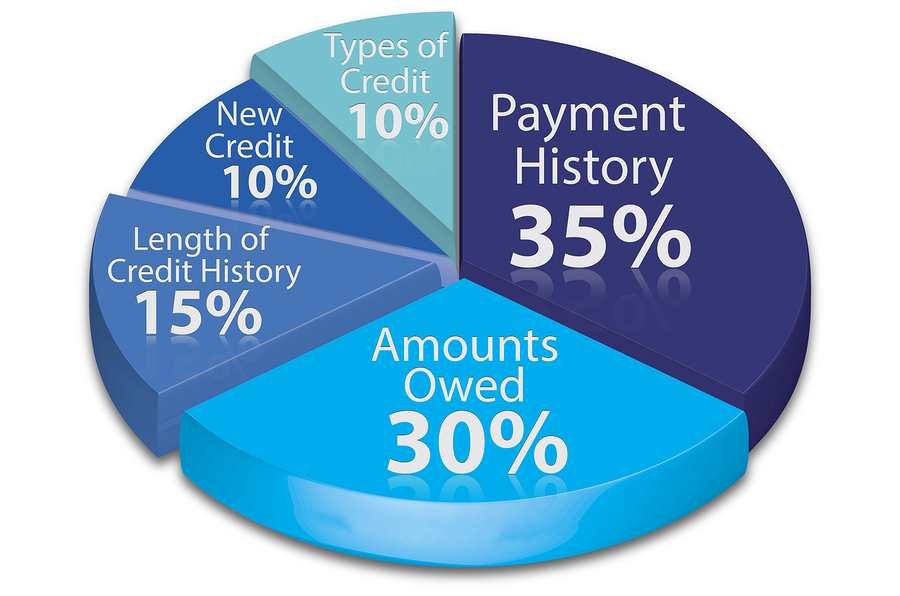

Understanding Your Credit Score Credit has become so essential to most big purchases you as a consumer will have to make, and that can be scary if you do not know how credit works. Credit can be confusing, but the more you can learn and utilize your credit effectively, the better off you will be […]