The average U.S. credit score has dipped to 715, according to FICO’s April 2025 Credit Score Insights. While this still falls within the “good” range, it marks a two-point drop year-over-year — the steepest decline since the Great Recession. For many Americans, this shift is more than just a number; it’s a signal that financial […]

Category Archives: Credit Repair Blogs

Collections, Credit Repair Blogs, Debt Collection, Scams

Debt Collection Letter for a Debt You Don’t Owe? Here’s What You Need to Do

30

Jun

Jun

Imagine opening your mailbox and finding a debt collection notice for an account you’ve never seen before. You don’t recognize the creditor. You never opened the account. Yet the collection agency claims you owe hundreds—or even thousands—of dollars. Unfortunately, this scenario is becoming increasingly common. At Credit Law Center, we regularly help consumers who discover […]

Credit Repair Blogs, Credit Score, Student Loans

Credit Scores Are Dropping Nationwide: Why Legal Credit Repair Matters More Than Ever

11

Jun

Jun

A strong credit score is the foundation of financial stability—impacting everything from mortgage approvals to affordable interest rates. But recent data reveals a troubling trend: credit scores are falling across multiple states, creating what experts call a “perfect storm” for American wallets. For consumers, this isn’t just a statistic—it’s a wake-up call. What’s Happening? According […]

Charge Off, Credit Cards, Credit Repair Blogs, Debt Negotiation

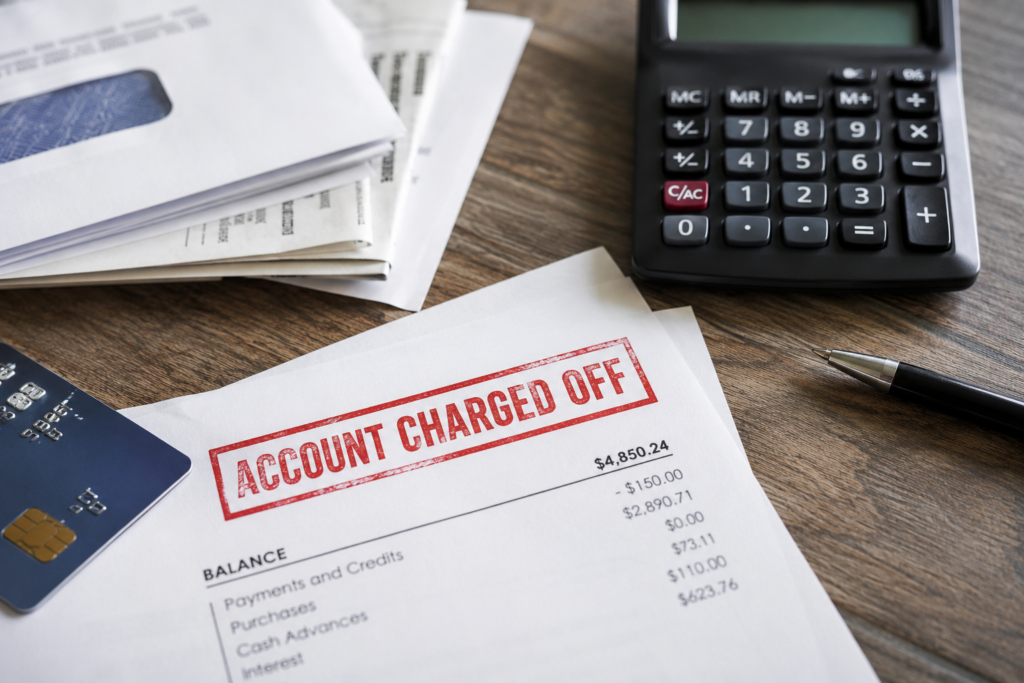

What Happens When Your Unpaid Credit Card Debt Gets Charged Off?

21

May

May

Falling behind on credit card payments can happen faster than many people expect. Rising living costs, high interest rates, medical expenses, and unexpected financial hardships have forced many Americans to rely more heavily on credit cards just to manage everyday expenses. Unfortunately, when payments are missed and balances continue to grow, the situation can quickly […]

30

Apr

Apr

How Do Negative Items Affect Me? Negative items on your credit report could be what separates you from that home loan you hoped for or a decent financing for a vehicle. The good news is that if you happen to have these negative items on your credit report, there are still wats to mitigate their […]

Credit Cards, Credit Optimization, Credit Repair Blogs, Credit Score

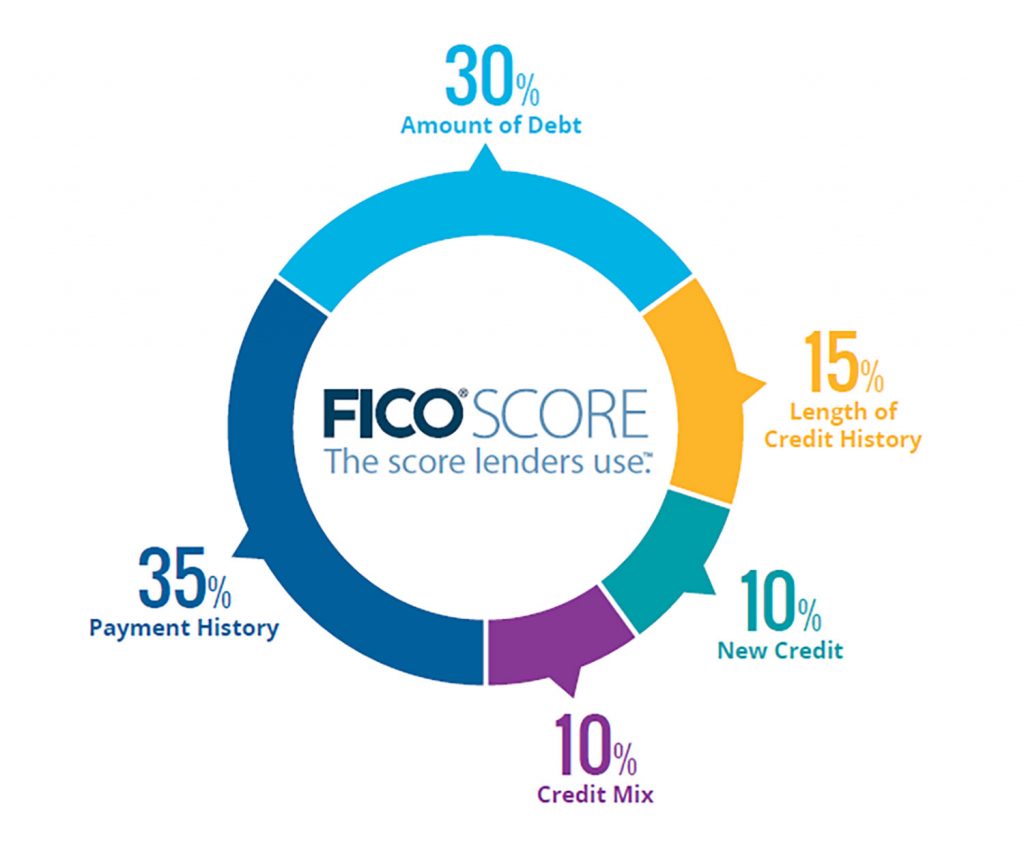

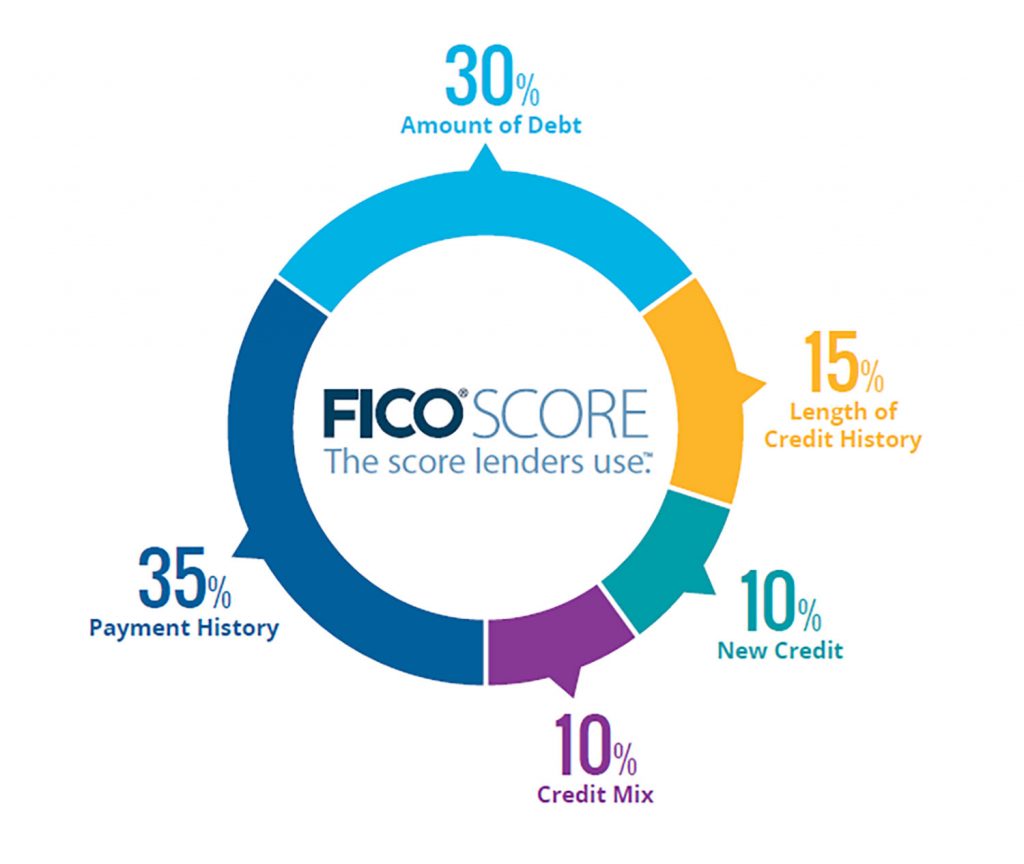

Why an 850 Credit Score Isn’t the Real Goal — And What Actually Matters

31

Mar

Mar

At Credit Law Center, we hear it all the time: “I want a perfect 850 credit score.” On paper, an 850 sounds impressive. It’s the highest score possible under the FICO® model and often treated as the gold standard of financial responsibility. But in practice, a perfect score is far less important—and far less useful—than […]

Building Credit, Credit Cards, Credit Repair Blogs, Debt Consolidation, Mortgage

How Falling HELOC Rates Are Creating New Credit Repair Opportunities for Homeowners

12

Mar

Mar

Over the past 18 months, a major financial shift has occurred that many homeowners may not have fully recognized: home equity in the United States has reached historic levels. For consumers struggling with high credit card balances or revolving debt, this development may present a powerful opportunity to strengthen their financial standing and improve their […]

13

Nov

Nov

There is a major difference between what a credit repair company can do versus what a law firm specializing in credit repair can. What you may find even more interesting is that a consumer can actually do more than what a credit repair company will. A Law Firm however, trumps all. We have been using the law […]

01

Jul

Jul

How Do Negative Items Affect Me? Negative items on your credit report could be what separates you from that home loan you hoped for or a decent financing for a vehicle. The good news is that if you happen to have these negative items on your credit report, there are still wats to mitigate their […]

16

Jun

Jun

As a law firm dedicated to credit repair and the protection of consumer rights, we understand the complexities surrounding credit reporting. In this article, we are going to focus to crucial components of the dispute process: Automated Consumer Dispute Verification (ACDV) and Automated Universal Dataform (AUD). Our commitment to educating consumers and advocating for their […]