How Do Negative Items Affect Me? Negative items on your credit report could be what separates you from that home loan you hoped for or a decent financing for a vehicle. The good news is that if you happen to have these negative items on your credit report, there are still wats to mitigate their […]

Tag Archives: credit repair

19

Feb

Feb

Why choose a Law Firm for Credit Repair? The fact is, there are many Credit Repair Organizations operating in the US right now. There are many good companies out there that have the best interest for their clients at heart. Then again, there are many who don’t. To be perfectly honest, there is no reason […]

13

Nov

Nov

There is a major difference between what a credit repair company can do versus what a law firm specializing in credit repair can. What you may find even more interesting is that a consumer can actually do more than what a credit repair company will. A Law Firm however, trumps all. We have been using the law […]

01

Jul

Jul

How Do Negative Items Affect Me? Negative items on your credit report could be what separates you from that home loan you hoped for or a decent financing for a vehicle. The good news is that if you happen to have these negative items on your credit report, there are still wats to mitigate their […]

15

May

May

The federal government resumed collections on defaulted federal student loans starting May 5, 2025, marking the first time in five years that such collections have restarted after pandemic-related pauses. This means the Department of Education can now garnish wages, tax refunds, and even Social Security benefits of borrowers whose federal student loans are in default—defined […]

24

Apr

Apr

Credit Alerts Worth Setting Up Now In order to maintain great credit scores, keeping track of all the activity on your accounts is key! Smart phones are attempting to make our lives easier with a multitude of applications. All major banking institutions now have online banking or apps to make life easier on their customers. […]

04

Feb

Feb

I remember sitting around a bonfire one cool autumn evening with a few close friends from high school. We had all gone our separate ways after graduation, some of us went to acquire our degrees immediately, others went off to the military and some went to trade schools to prepare themselves for an apprenticeship. As […]

06

Nov

Nov

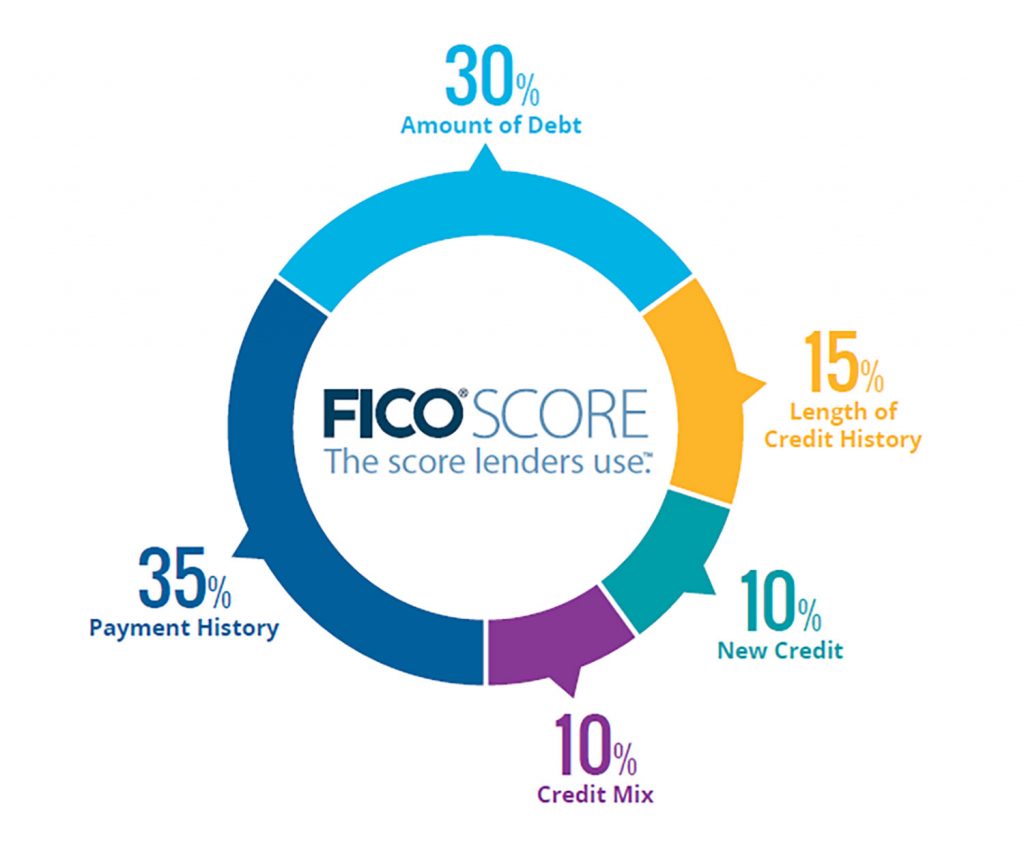

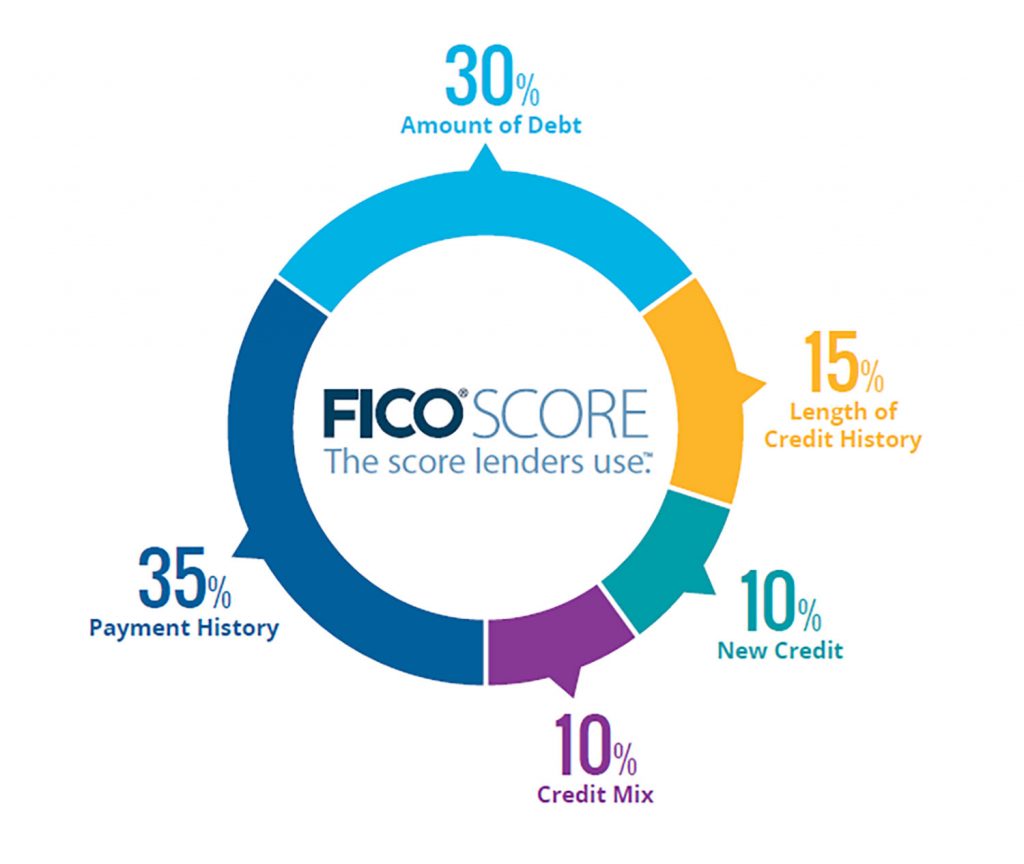

Your Fix of the Mix We all know the importance of having a good credit score. With a high credit score, you can open to door to better interest rates, loans, benefits and more! Good credit can be the deciding factor in whether or not you get approved to rent a home or get a […]

16

Jul

Jul

I remember sitting around a bonfire one cool autumn evening with a few close friends from high school. We had all gone our separate ways after graduation, some of us went to acquire our degrees immediately, others went off to the military and some went to trade schools to prepare themselves for an apprenticeship. As […]

26

Oct

Oct

Why choose a Law Firm for Credit Repair? The fact is, there are many Credit Repair Organizations operating in the US right now. There are many good companies out there that have the best interest for their clients at heart. Then again, there are many who don’t. To be perfectly honest, there is no reason […]