The average U.S. credit score has dipped to 715, according to FICO’s April 2025 Credit Score Insights. While this still falls within the “good” range, it marks a two-point drop year-over-year — the steepest decline since the Great Recession. For many Americans, this shift is more than just a number; it’s a signal that financial […]

Tag Archives: attorney based credit repair

Charge Off, Credit Cards, Credit Repair Blogs, Debt Negotiation

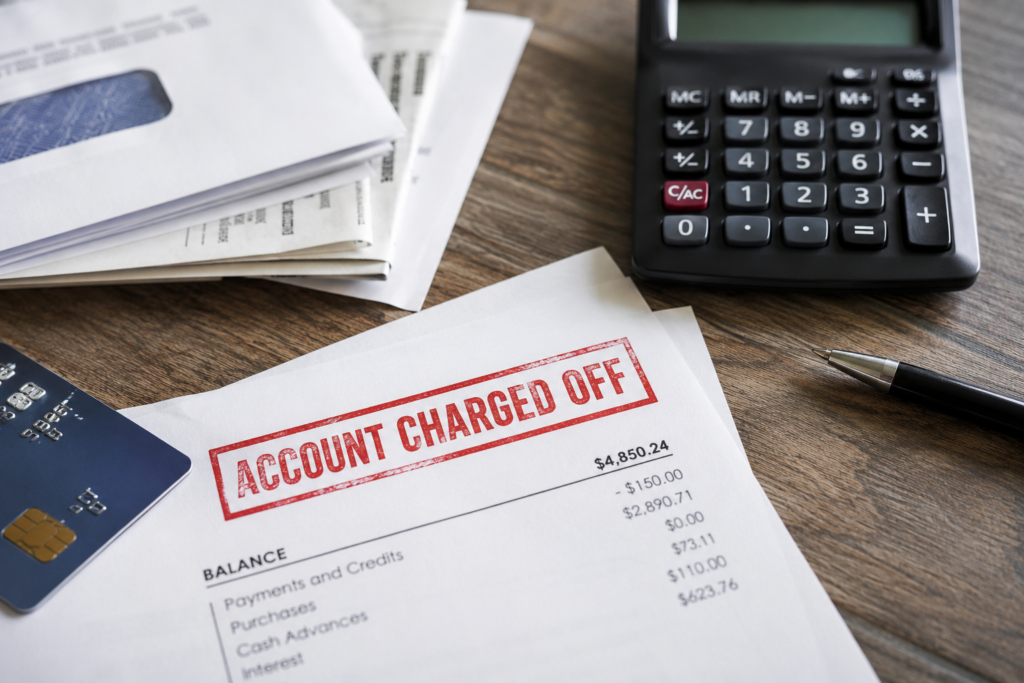

What Happens When Your Unpaid Credit Card Debt Gets Charged Off?

21

May

May

Falling behind on credit card payments can happen faster than many people expect. Rising living costs, high interest rates, medical expenses, and unexpected financial hardships have forced many Americans to rely more heavily on credit cards just to manage everyday expenses. Unfortunately, when payments are missed and balances continue to grow, the situation can quickly […]

19

Feb

Feb

Why choose a Law Firm for Credit Repair? The fact is, there are many Credit Repair Organizations operating in the US right now. There are many good companies out there that have the best interest for their clients at heart. Then again, there are many who don’t. To be perfectly honest, there is no reason […]

26

Oct

Oct

Why choose a Law Firm for Credit Repair? The fact is, there are many Credit Repair Organizations operating in the US right now. There are many good companies out there that have the best interest for their clients at heart. Then again, there are many who don’t. To be perfectly honest, there is no reason […]

20

Jul

Jul

The Why: Phoenix Financial Services attempted to collect on debts that were disputed by consumers and using unlawful letters and misrepresentations to attain these collections. The CFPB took action against Phoenix Financial for numerous debt collection and credit reporting violations. In over a thousand cases, this collection company continued to collect on a debt […]

02

May

May

This is really not breaking news at this point. It’s been happening for a couple of years now. But I do think it worth mentioning again. Debt Collection companies CAN try and collect via your social media accounts. Over time, our communication process has changed dramatically. The idea of making a phone call when […]

30

Mar

Mar

Why choose a Law Firm for Credit Repair? The fact is, there are many Credit Repair Organizations operating in the US right now. There are many good companies out there that have the best interest for their clients at heart. Then again, there are many who don’t. To be perfectly honest, there is no reason […]

05

Jan

Jan

How Long Is This Going To Take? Credit repair seems like a long and tedious process, but have you ever wondered why it takes to long to complete? Many people often look to repair their credit with a specific goal in mind (like taking out a car lone or purchasing a house) it’s important to […]

05

Jan

Jan

How Long Is This Going To Take? Credit repair seems like a long and tedious process, but have you ever wondered why it takes to long to complete? Many people often look to repair their credit with a specific goal in mind (like taking out a car lone or purchasing a house) it’s important to […]

07

May

May

Why Consumers Hire a Law Firm For Credit Repair There is a major difference between what a credit repair company can do versus what a law firm specializing in credit repair can. What you may find even more interesting is that a consumer can actually do more than what a credit repair company will. A […]