How Your Score Is Costing You Thousands Back when I graduated high school (a few years after dinosaurs walked the earth) I had absolutely no idea how detrimental my credit score would be to my future purchases. My brother was sitting pretty with a 750 credit score and financed his new car at an extremely […]

Tag Archives: FICO

03

Oct

Oct

As a law firm specializing in credit repair and consumer financial rights, we view FICO’s launch of the Mortgage Direct License Program as a pivotal moment in the evolution of credit scoring transparency and affordability—especially in the mortgage industry. Historically, consumers have been subject to opaque pricing structures and limited access to the mechanisms that […]

17

Jul

Jul

The next chapter in the Medical Debt Saga. In January 2025, the Consumer Financial Protection Bureau (CFPB) finalized a rule that would have removed medical debt from credit reports and prohibited lenders from using medical information in credit decisions. The rule aimed to help around 15 million Americans and eliminate about $49 billion in medical debt from credit reports. It was […]

17

Jul

Jul

I Want To Buy, Now! Are you preparing to purchase a home in the next few months? It seems that when we are not looking, a home just pops up and finds us, at a time when we were not even contemplating making a move. Then, boom! The rush is on to beat the clock […]

29

Oct

Oct

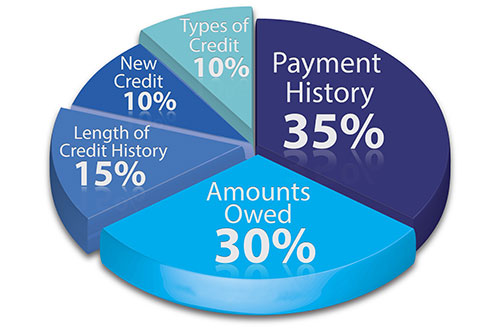

Building Up Your FICO Understanding and building credit in a positive way takes discipline and some education. Do you recall being taught in school, how to build your credit scores? Did your teachers let you know how big of a role credit would play in your life as you got older? Honestly, it is probably […]

08

Aug

Aug

Are you preparing to purchase a home in the next few months? It seems that when we are not looking, a home just pops up and finds us, at a time when we were not even contemplating making a move. Then, boom! The rush is on to beat the clock and make an offer before […]

03

Aug

Aug

To piggyback on our last blog, a statement from the National Consumer Reporting Association (NCRA) sounded the alarm of sharp price increases for purchasing credit reports. The surprising fact to me is the vast discrepancies in who is charged and at what percentage the charges will increase. The NCRA stated, “the vast majority of mortgage […]

01

Aug

Aug

Last week the Community Home Lenders of America (CHLA) penned a letter to the Federal Housing Finance Agency (FHFA) stating that the pending addition of updated Credit Scores at Fannie Mae and Freddie Mac could be more manageable if done one at a time. Specifically, they stated the need to add VantageScore first. This is […]

11

May

May

I have clients from all over the country asking me how much particular items on their credit report are affecting their credit and if the item is removed, then will their credit score rise. It is difficult to provide a precise answer because there are many underlying factors that can make or break your credit! […]

30

Oct

Oct

Building Up Your FICO Understanding and building credit in a positive way takes discipline and some education. Do you recall being taught in school, how to build your credit scores? Did your teachers let you know how big of a role credit would play in your life as you got older? Honestly, it is probably […]