Good, Better, Best and Bad The internet and cell phones have now made it easier than ever to check your credit score as often as you’d like. Millennials are starting to check their credit scores more frequently than any other generation. This could be due to the fact that credit has become vital in many […]

Charge Off, Credit Cards, Credit Repair Blogs, Debt Negotiation

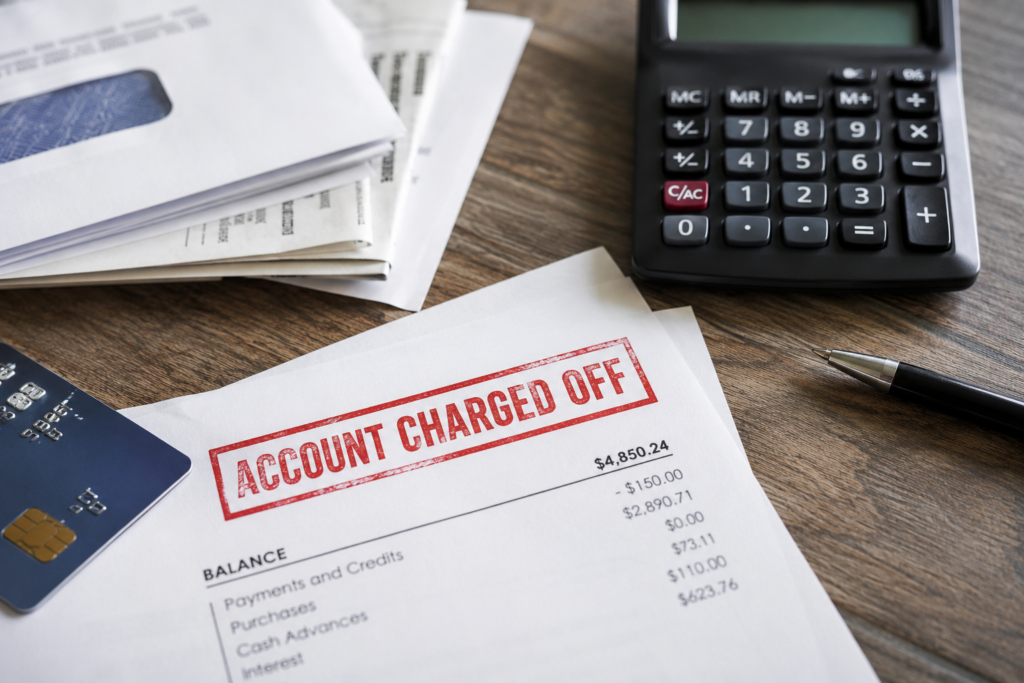

What Happens When Your Unpaid Credit Card Debt Gets Charged Off?

21

May

May

Falling behind on credit card payments can happen faster than many people expect. Rising living costs, high interest rates, medical expenses, and unexpected financial hardships have forced many Americans to rely more heavily on credit cards just to manage everyday expenses. Unfortunately, when payments are missed and balances continue to grow, the situation can quickly […]

Credit Score

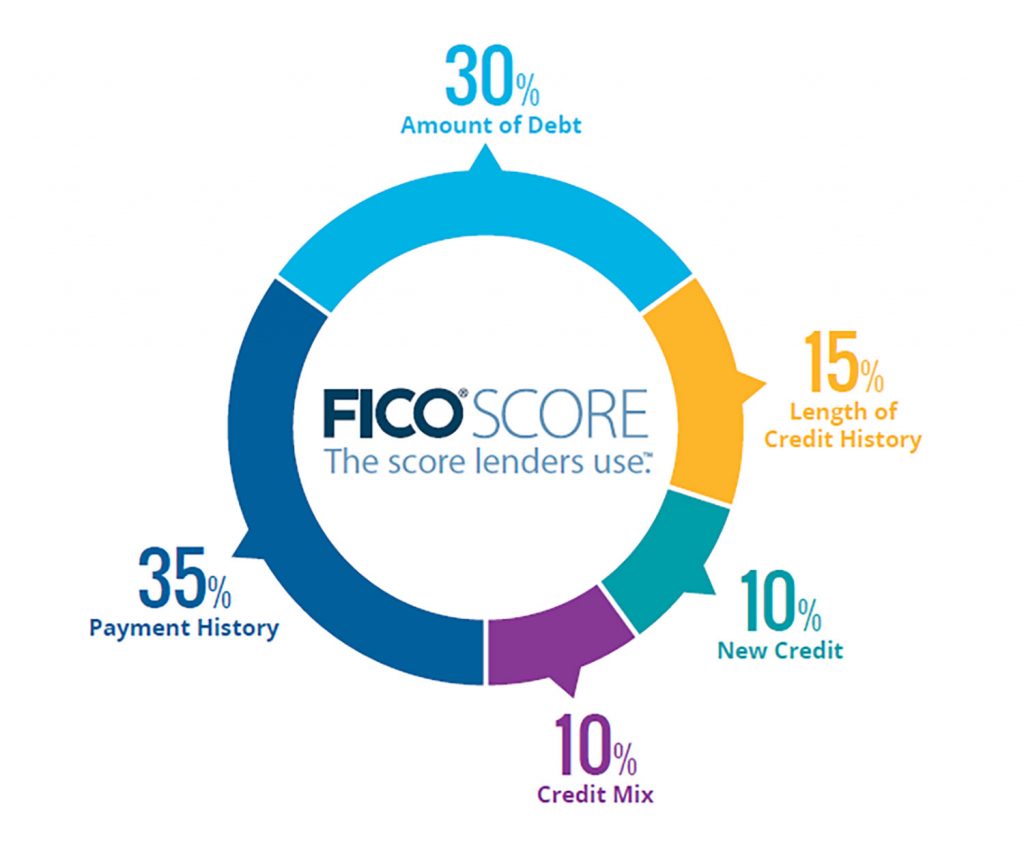

FICO vs. VantageScore: Why You Have More Than One Credit Score — And Which One Matters for a Mortgage

19

May

May

Most consumers think they have “a credit score.” In reality, you probably have dozens. That’s because multiple companies create credit scoring models, and each model can generate different versions depending on the type of lending involved. The two biggest players in the industry are FICO and VantageScore. While both companies use information from your credit […]

14

May

May

There is a growing trend for alternate lending sweeping the country for those that may not be able to gain funding from traditional avenues; Buy Now Pay Later. There are some very good reasons to go this route. However, like any other options for purchasing, there are some pitfalls as well. Is it a good […]

05

May

May

With household debt at record highs, many Americans are searching for a way out of overwhelming credit card balances. Debt relief companies often position themselves as a solution, promising reduced balances and a path to financial freedom. But what many consumers don’t fully understand is how these programs actually work — and the risks involved. […]

30

Apr

Apr

How Do Negative Items Affect Me? Negative items on your credit report could be what separates you from that home loan you hoped for or a decent financing for a vehicle. The good news is that if you happen to have these negative items on your credit report, there are still wats to mitigate their […]

28

Apr

Apr

Your credit score isn’t just a number—it’s a key that unlocks financial opportunities. From qualifying for a mortgage to getting approved for a credit card, your score impacts nearly every major financial decision. Yet, most people don’t know how their score compares to others in their age group—or what steps they can take to improve […]

21

Apr

Apr

Let’s be real—saving money when your paycheck barely covers the essentials can feel like trying to fill a bucket with a hole in it. But here’s the truth: it’s not about how much you make, it’s about what you do with what you have. Whether you’re working a minimum-wage job or juggling multiple gigs, there […]

16

Apr

Apr

Most all of us have heard of Debt consolidation. But is Debt Consolidation right for you? What type of debt consolidation should one choose? Is Debt Consolidation effective? What are some of the pitfalls of debt consolidation? Guess what, sometimes “life” happens and we need to utilize our credit cards out of necessity. A perfect […]

Collections, Debt Collection

Debt Collectors Want a Reset. Courts—and Consumer Protection Law—Say Not So Fast.

14

Apr

Apr

Source: Site At Credit Law Center, we’ve seen this pattern before: a major debt collector gets caught violating consumer protection laws, agrees to a settlement, and then—once the spotlight fades—tries to walk it back. That’s exactly what’s happening right now. Portfolio Recovery Associates (PRA Group) is asking a federal court in Virginia to undo or […]