Building Up Your Fico Understanding and building credit in a positive way takes discipline and some education. Do you recall being taught in school, how to build your credit scores? Did your teachers let you know how big of a role credit would play in your life as you got older? Honestly, it is probably […]

Tag Archives: infographic

10

Jul

Jul

Credit Card Debt & Balance Transfers Where is your credit card debt currently at? Are you making minimum payments that don’t make a dent once your interest rates kicked in? It may be time to weigh a different option now that you are hoping to make some headway on your current debts. Your Balances and […]

05

Jul

Jul

Credit Scores Dropping Have you noticed a random decrease in your credit scores recently? There are many factors that can cause your credit scores to fluctuate. Many consumers do not understand that a credit score has no memory and can change immediately due to activity or changes that can happen as soon as you make […]

03

Jul

Jul

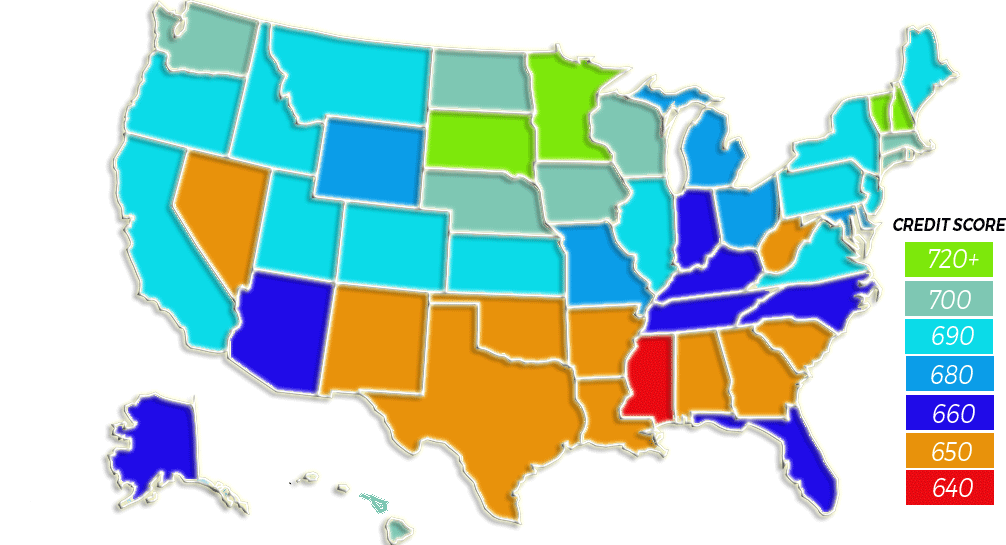

Battle of the States Have you ever wondered what part of the United States has the best/worst credit scores? It may come as a surprise to you but, the highest scoring state, Minnesota has an average credit score of 709. What may come as even more of a shock is that yes, they do have […]

22

Jun

Jun

5 Ideas for Smart Summer Savings The first day of Summer officially arrived although it seems we have skipped most of Spring this year! Have you noticed your bills are much higher than the previous Summer? It’s no surprise that while the days are longer and hotter, utility bills are headed on up too. We […]

19

Jun

Jun

How To Deal With Debt Collectors I have recently been receiving strange calls from someone trying to collect money from me, what do I do? As a consumer, it is important to be educated about the process by which an actual collection agency attempts to collect debts as opposed to scam callers asking you to […]

15

Jun

Jun

Increased Credit Scores by 100 Points At Credit Law Center we love hearing success stories from past clients. One client shares how Credit Law Center helped her family save money and increase their scores. What brought you to Credit Law Center? I was online one day and was looking at homes. A lender reached out […]

14

Jun

Jun

Impact of Timeshares on Credit Reports A timeshare can be something that affects your credit scores. When thinking about purchasing a timeshare, consider it to be as vital and possibly as damaging as a mortgage to your credit report. There are many variables that come into purchasing a timeshare. If your family is tossing around […]

- 1

- 2